Space Computing Race Heats Up: China Builds Institutional Framework, Space Computing Infrastructure Accelerates

2026 June — China is laying the institutional groundwork for a "space computing" infrastructure race with rare organizational mobilization. According to the latest report from SpaceNews, Beijing is building a comprehensive industrial policy framework to support the construction of space computing infrastructure, with a series of influential coordinating bodies emerging. This is not merely a tactical upgrade of China's space strategy — it could fundamentally reshape the geography of global cloud computing and AI infrastructure.

I. Anatomy of the Framework: How Institutions Drive Space Computing

China's space computing policy framework is not a single document or announcement, but consists of a three-layer structure:

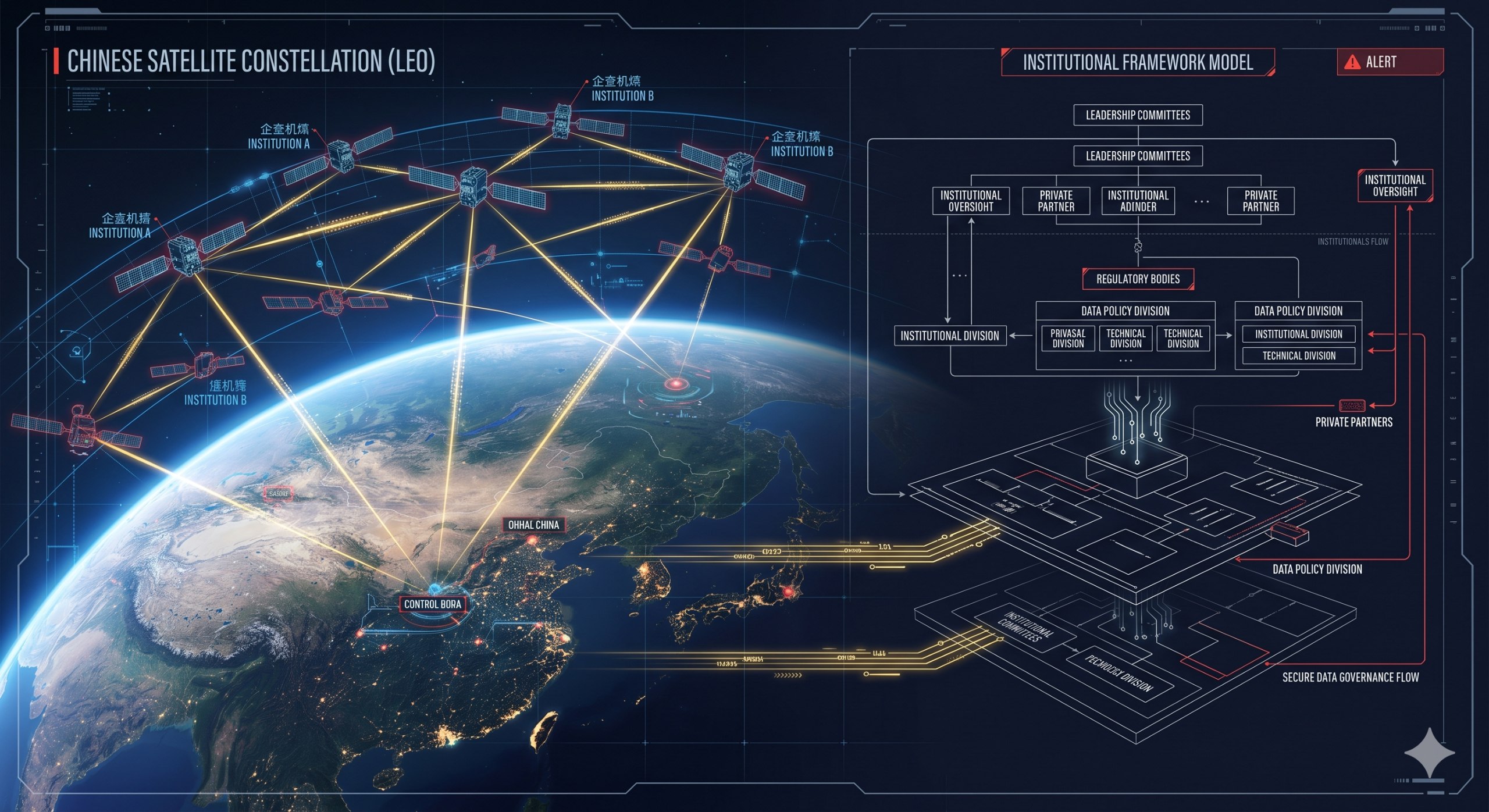

1. Top-Level Coordinating Body The newly established "National Space Computing Leadership Group" (provisional name) reports directly to the Central Committee for Civil-Military Integration Development, coordinating resources across the Ministry of Industry and Information Technology, the China National Space Administration, the Chinese Academy of Sciences, and multiple state-owned aerospace enterprises. The group's responsibilities include formulating space computing technology roadmaps, coordinating constellation spectrum resources, and approving major demonstration projects — similar to the cross-departmental coordination mechanism that drove the BeiDou satellite navigation system, but at a higher level and faster pace.

2. Industrial Technology Roadmap The "National Space Computing Infrastructure Development Plan (2026–2035)" released in early 2026 clearly articulates a three-phase roadmap:

- Near-term (2026–2028): Complete key technology verification, including on-orbit AI inference chips, inter-satellite laser links, and space-grade data center thermal management systems

- Mid-term (2029–2032): Deploy the first medium and low orbit hybrid computing constellation, providing 10–100 PFLOPS of aggregate on-orbit computing power

- Long-term (2033–2035): Build a globally covered space computing network, achieving seamless integration with ground-based computing infrastructure

3. Key Laboratories and Industry Alliances The Chinese Academy of Sciences Center for Space Application and Engineering has led the establishment of the "Space Computing Technology Innovation Alliance," with members including CASC, CASIC, Huawei, ZTE, and several AI chip startups. Additionally, the "Joint Laboratory for Space Computing," jointly established by the University of Science and Technology of China and the National University of Defense Technology, began operations in late 2025, focusing on onboard GPU architecture and radiation-hardened chip design.

II. Why Put Computing Power in Space?

The driving forces behind space computing are fundamentally different from ground-based data centers, with strategic logic built on three core advantages:

Latency Advantage For globally distributed users, low Earth orbit (LEO) computing nodes can compress data round-trip time to 10–20 milliseconds, far below the 100–300 milliseconds of intercontinental fiber optics. For real-time AI inference (autonomous driving, remote surgery, defense early warning), this latency difference is decisive.

Unconstrained Energy and Space On the ground, data centers face increasingly severe challenges from power supply shortages, water consumption, land acquisition, and environmental permitting. The space environment offers:

- Continuous uninterrupted solar power (persistent generation on the sun-facing side without batteries)

- Natural radiative cooling (efficient heat dissipation in vacuum)

- Nearly unlimited expansion space

Orbital Edge Computing Satellites generate hundreds of terabytes of Earth observation and communications data daily. The current model transmits all data down to ground stations for processing — bandwidth bottlenecks and latency issues are growing increasingly acute. The core concept of space computing is: complete data processing and AI inference directly in orbit, transmitting only meaningful results back to Earth. This has direct tactical value for China's remote sensing satellite constellations (Gaofen series, Jilin-1, etc.).

III. China's Existing Infrastructure: Where Is the Starting Point?

China's development of space computing does not start from zero. After two decades of sustained investment, China has built the world's second-largest space infrastructure system:

Tiangong Space Station As the only independently operating space station currently in orbit (outside the ISS cooperation framework), Tiangong provides a unique "space computing experimental platform." The "Space Application System" aboard the Mengtian experiment module has supported multiple on-orbit computing experiments, including:

- On-orbit edge inference tests based on domestic chips (Loongson, Phytium)

- Satellite-ground quantum communication and encrypted computing verification

- Space robot autonomous mission planning algorithms

Mega Satellite Constellations

- Qianfan Constellation (G60 Starlink): Led by Shanghai Yuanxin Satellite, planning over 15,000 satellites, with the first 648 deployed in 2024–2025. Qianfan's goal is not only communication but also includes edge computing node functions.

- Guowang Constellation: Operated by SatNet, approximately 13,000 satellites, focusing on high-throughput communications and specialized communications. Its distributed node architecture is naturally suited for evolution into a computing constellation.

- Remote Sensing and Science Satellite Fleet: The Gaofen series, Fengyun series, and CAS-led "Taiji-1" gravitational wave detection satellite have accumulated extensive onboard data processing experience.

Rocket Launch Capacity The Long March 5B, Long March 8, and the Long March 9 (heavy-lift rocket, Starship-class) under development provide launch support for large-scale constellation deployment. Reusable rockets in the commercial space sector (such as LandSpace's Zhuque-3 and Galactic Energy's Pallas-1) are also accelerating, with orbital recovery expected in 2027–2028.

IV. US-China Competition: Comparing Two Approaches

China's space computing framework does not develop in isolation. Benchmarking against equivalent US efforts provides clearer insight into the nature of this competition.

| Dimension | US (Muon Space / Starcloud etc.) | China (Policy Framework) |

|---|---|---|

| Driving Entity | Private enterprise-led (Muon, Starcloud, Lumen Orbit) | State-led, state-owned + private enterprise collaboration |

| Core Platform | Condor-Ultra (20–100kW satellite platform), NVIDIA Space-1 Rubin GPU | Under planning, Tiangong as experimental platform, Qianfan/Guowang as deployment carriers |

| AI Chip | NVIDIA Vera Rubin (25x H100 performance) | Domestic AI chips (Cambricon, Huawei Ascend, NUDT self-developed radiation-hardened solutions) |

| Deployment Timeline | 2028 first Condor-Ultra path verification | 2026–2028 key technology verification, 2029–2032 small-scale deployment |

| Launch Vehicle | SpaceX Starship (fully reusable, low cost) | Long March 9 (under development) + commercial reusable rockets (2027–2028) |

| Business Model | Satellite Platform as a Service (SPaaS), serving hyperscalers | Hybrid model: communication + remote sensing + computing integration, national security priority |

| Coordination Mechanism | Market-driven competition, no unified coordination | Cross-department leadership group unified planning, civil-military integration driven |

The key difference: the US path is "thinner" — starting from select application scenarios (AI inference), driven by venture capital enabling rapid iteration; China's path is "thicker" — embedding space computing into the overall layout of communications, remote sensing, and defense, with long-term institutional investment.

Muon Space's Condor-Ultra first flight in 2028 is seen as a litmus test for the US approach. Meanwhile, China's Qianfan constellation has already accumulated over 600 nodes in orbit — while these nodes currently primarily carry communication functions, their hardware architecture has reserved sufficient margin for future upgrade to computing nodes.

V. Strategic Implications: A New Dimension of Tech Competition

The emergence of the space computing framework expands tech competition from the ground to an entirely new dimension:

1. "De-terrestrialization" of AI Computing Power If space computing nodes prove viable, the infrastructure landscape of global AI inference will be redrawn. For Southeast Asia, Africa, and South America — regions lacking large-scale ground data centers — space computing could become a "leapfrog" path bypassing traditional infrastructure development stages. China's space cooperation relationships with developing countries established through the Belt and Road framework (such as the Egypt Satellite Assembly and Testing Center, the China-Brazil Earth Resources Satellite) could become early international customer networks for its space computing services.

2. Deepening of Civil-Military Integration The value of space computing in military application scenarios is self-evident: real-time battlefield situational awareness, distributed command and control, autonomous unmanned system coordination. China's civil-military integration system creates a much shorter path from laboratory to application compared to the US — where institutional friction between ITAR regulations and commercial confidentiality protection persists.

3. Contest for Standard-Setting Power Whoever dominates the technical standards for space computing (inter-satellite communication protocols, data formats, security architecture) may control the rule-setting power of the next-generation space economy. China's experience in 5G, blockchain, and IoT standard-setting — forming de facto standards through a large domestic market, then promoting them internationally through the Belt and Road mechanism — is highly likely to be replicated in the space computing domain.

4. Launch Cost Asymmetry Risk China's biggest bottleneck for space computing is not in space, but on the ground: launch vehicles. Starship's fully reusable design aims to reduce per-kilogram launch costs below $200, while China's Long March 9, though comparable in performance, is still years away from its first flight. During 2027–2028, when Starship becomes operational, the US may gain a 2–3 year window of launch cost advantage. This means China needs to use the "acceleration" of institutional efficiency to compensate for the "disadvantage" in launch costs during this window.

VI. Timeline and Milestones

The following is a projected timeline based on publicly available information and industry analysis:

| Time | Expected Milestones |

|---|---|

| 2026 Q3–Q4 | Details of the "Space Computing Infrastructure Development Plan" released; first round of space computing pre-research project bidding |

| 2027 H1 | On-orbit AI inference chip prototype completes ground testing; Qianfan constellation launches first batch of new-generation satellites with edge computing capability |

| 2027 H2 | Tiangong space station completes large-scale on-orbit computing experiments; National Space Computing Leadership Group releases first annual assessment report |

| 2028 H1 | Long March 9 heavy-lift rocket first orbital test (if on schedule); Muon Space Condor-Ultra first flight (US benchmark) |

| 2028–2029 | China's first dedicated space computing experimental satellite launched; Qianfan/Guowang second-generation nodes integrate computing units |

| 2029–2030 | First medium and low orbit hybrid computing constellation (~10 satellites) on-orbit verification; aggregate computing power reaches 10 PFLOPS |

| 2030–2032 | Small-scale commercial pilot programs (targeting Southeast Asia/Africa customers) |

| 2033–2035 | Global coverage space computing network initially established, integrated with ground computing infrastructure |

VII. Observations and Conclusions

The formation of China's space computing framework is the clearest signal yet: space is no longer just a battleground for communications and remote sensing — computing is becoming the third commercially viable space infrastructure layer. Unlike the US path driven by enterprises and capital, China's institutional mobilization model offers an alternative approach "from planning to execution" — it may start slower, but once launched, the concentration of resources and consistency of execution will generate enormous cumulative effects.

The real focus of competition is not who deploys the first space computing node, but who can most effectively integrate space computing power into their overall technology ecosystem — from AI model training and inference, to global IoT, autonomous driving, and defense early warning. In this race, hardware capability is only the starting point; ecosystem integration is the final destination.

POC.HK will continue to track technology, policy, and business developments in the space computing field, providing readers with in-depth observations.