The AI IPO Superwave: Anthropic, OpenAI, SpaceX, and the Structural Transformation of Technology Finance

POC.HK Future Technology Observatory Research Report

June 2026

Table of Contents

Chapter 1: Introduction — The Week That Changed Tech Finance Chapter 2: Anthropic — A $965 Billion Validation of the Safety-First Approach Chapter 3: OpenAI — From Non-Profit to $852 Billion Public Giant Chapter 4: Titans Compared — Business Models, Risks, and Valuation Logic Chapter 5: SpaceX — The $1.77 Trillion Elephant in the Room Chapter 6: Capital Rotation Effects — Impact on FAANG and Tech Markets Chapter 7: AI IPO as Industry Signal — How Public Markets Price AI Maturity Chapter 8: Regulation and Antitrust — SEC, EU AI Act, and AI Governance Chapter 9: The Post-IPO AI Landscape — Winners, Losers, and a New Ecosystem Chapter 10: Conclusion — Investing in the AI Infrastructure Transition

Chapter 1: Introduction — The Week That Changed Tech Finance

The twelve days from May 28 to June 8, 2026, may be the most consequential period in technology finance history.

Within these twelve days, three companies — Anthropic, OpenAI, and SpaceX — with a combined valuation exceeding $3.5 trillion, took decisive steps toward the public market nearly simultaneously. Anthropic completed a $65 billion Series H round (at a $965 billion valuation) and immediately filed a confidential S-1 with the SEC. One week later, OpenAI submitted its own confidential IPO filing (at an $852 billion valuation). Between them, SpaceX was advancing its IPO process at a $1.77 trillion valuation and announced it would open allocations to retail investors.

This is not merely a collection of coincidental capital markets events. These three companies represent different facets of the same historical trend: the transition of AI from laboratory technology to commercial infrastructure, and the transition of space from government monopoly to commercial market. Their simultaneous emergence means the venture-capital-driven model of the past decade is giving way to a public-market-based model of scale realisation.

This report aims to deeply analyse the driving forces, market impacts, and long-term structural implications of this AI IPO wave. We examine the IPO paths of Anthropic, OpenAI, and SpaceX individually, compare their business models and valuation logic, analyse the capital rotation effects on existing tech giants, and forecast the post-IPO AI industry landscape.

Chapter 2: Anthropic — A $965 Billion Validation of the Safety-First Approach

Figure 1: Anthropic's safety-first positioning — a digital shield protecting enterprise AI infrastructure.

2.1 From Safety Research Lab to AI Giant

Anthropic's story begins in 2021, when a group of researchers dissatisfied with OpenAI's direction — including Dario Amodei (CEO) and Daniela Amodei (President) — decided to create a company with AI safety as its core mission. At the time, this was considered an idealistic choice: in AI, safety research was often seen as a brake on innovation rather than an engine of value creation.

Five years later, Anthropic became the world's most valuable AI startup at a $965 billion valuation, proving that safety is not merely compatible with commercialisation but has become the differentiating attribute enterprise customers are most willing to pay for.

2.2 Series H: The IPO Valuation Anchor

On May 28, 2026, Anthropic announced the completion of a $65 billion Series H round, led by Altimeter Capital, Dragoneer, Greenoaks, and Sequoia Capital. The post-money valuation of $965 billion instantly surpassed OpenAI's $852 billion record, making Anthropic the highest-valued AI company.

The scale and timing of this round are strategically significant. The $65 billion round — one of the largest single financing rounds in AI history — occurred just one week before Anthropic filed its IPO paperwork. This is not coincidence. The Series H round provided a valuation anchor for the IPO: by establishing a $965 billion price in the private market with the world's top venture investors, Anthropic signals to public market investors that this price has been validated by the most sophisticated capital allocators.

The investor lineup itself merits analysis. Altimeter Capital and Dragoneer are growth-stage investment firms whose participation typically precedes near-term liquidity events (i.e., IPOs). Sequoia Capital's continued participation reflects confidence in Anthropic's long-term value.

2.3 The Remarkable Growth Curve

Anthropic's S-1 filing reveals staggering growth numbers: as of May 2026, the company's annualised revenue run rate (ARR) reached $47 billion — nearly quintupling its $10 billion ARR at the end of 2025.

The primary drivers of this growth are twofold:

Claude 4 Opus Enterprise Penetration: Released in early 2026, Claude 4 Opus comprehensively surpassed GPT-4o in reasoning, code generation, and multimodal understanding. More importantly, Anthropic's Constitutional AI training methodology — which aligns model behaviour with a predefined set of principles — became the deciding factor for enterprise customers choosing Anthropic. For highly regulated industries such as financial services, healthcare, and government, model explainability and safety matter more than raw performance.

Fable 5 Market Positioning: Released in May 2026, Fable 5 represents Anthropic's latest breakthrough in reasoning capability. Unlike traditional conversational models, Fable 5 focuses on complex multi-step reasoning tasks, demonstrating capabilities exceeding human experts in mathematical proof, legal analysis, and scientific research. Anthropic positions Fable 5 as an "expert co-pilot," priced at $15 per million tokens — five times the price of Claude 4 Opus.

2.4 Revenue Structure and Profitability

Anthropic's revenue structure underwent a significant shift in 2026. In 2025, approximately 70% of revenue came from API calls (usage-based pricing) and 30% from enterprise contracts. By Q1 2026, this ratio had inverted to 40% API versus 60% enterprise contracts. This shift reflects the AI market's transition from experimental use to production-grade deployment — enterprise customers increasingly prefer annual contracts to lock in pricing and capacity rather than flexible usage-based arrangements.

However, Anthropic remains unprofitable. The company's 2025 operating loss was approximately $8-10 billion, primarily driven by massive investment in computing infrastructure. The company currently operates clusters exceeding 1 million GPUs (primarily NVIDIA H100/B200 and custom TPUs), with annual computing costs exceeding $15 billion.

Risk factors disclosed in the S-1 filing include: dependence on NVIDIA GPU supply (particularly uncertainty around export control policies), regulatory penalties from AI safety incidents, and rising compensation costs from talent competition.

→ Return to TOC | → Next: OpenAI

Chapter 3: OpenAI — From Non-Profit to $852 Billion Public Giant

Figure 2: OpenAI's dual structure — governance tension between the non-profit parent and for-profit public entity.

3.1 OpenAI's Journey of Transformation

OpenAI's story is longer, more曲折, and more controversial than Anthropic's. Founded in 2015 as a non-profit organisation with the mission of "ensuring that artificial general intelligence benefits all of humanity," OpenAI created a "capped-profit" structure — OpenAI LP — in 2019 that allowed outside investors to receive returns of up to 100x. In 2024, the company completed its structural transformation to a fully for-profit entity, clearing the legal path for an IPO.

This transformation was not smooth. The November 2023 board coup — in which CEO Sam Altman was briefly fired and then reinstated — exposed deep contradictions in OpenAI's governance structure: the conflict of interest between a non-profit board and a for-profit business. This event triggered the departure of several key researchers (many of whom joined Anthropic) and accelerated OpenAI's shift to a for-profit structure.

3.2 $122 Billion Raise: The Largest Private Fundraise in History

On March 31, 2026, OpenAI completed the largest private fundraise in human history — $122 billion at an $852 billion valuation. The scale of this round exceeds the GDP of many nations, reflecting the capital intensity of AI infrastructure.

The investor lineup itself is an industry signal:

- Amazon: Committed $50 billion, becoming OpenAI's largest strategic investor. This investment creates an interesting dynamic with Amazon's own AI efforts (AWS Bedrock, Alexa, custom Trainium chips) — Amazon is simultaneously an AI infrastructure supplier and one of the largest consumers of AI models.

- NVIDIA: Committed $30 billion in a combination of product credits and cash. NVIDIA's investment is both a financial bet and a strategic supply chain consolidation — OpenAI is one of NVIDIA's largest single GPU customers.

- SoftBank: Committed $30 billion, continuing Masayoshi Son's aggressive investment style in AI. SoftBank's participation provides long-term capital support while offering a potential exit channel for SoftBank's Vision Fund.

Combined with previous rounds, OpenAI's cumulative fundraising has reached $180 billion — making it the most heavily funded startup in human history.

3.3 Revenue Model and Unit Economics

OpenAI's revenue model is more diversified than Anthropic's:

ChatGPT Subscriptions: Contributing approximately 45% of revenue. ChatGPT's paid users exceeded 50 million in Q1 2026, spanning three tiers: Plus ($20/month), Pro ($200/month), and Team ($25/user/month), covering needs from individual to enterprise.

API Services: Contributing approximately 40% of revenue. OpenAI's API ecosystem has over 3 million developers, covering multiple model tiers from GPT-4o (general conversation) to o3-pro (deep reasoning).

Enterprise Solutions: Contributing approximately 15% of revenue but growing fastest. OpenAI Enterprise signed over 500 Fortune 500 companies in 2026, primarily concentrated in three verticals: customer service automation, code generation, and data analysis.

OpenAI's unit economics are improving. In 2025, every $1 of API revenue carried approximately $0.85 in computing costs, yielding a gross margin of only 15%. By Q1 2026, with o3-pro's premium pricing ($0.15/1K tokens, approximately 3x GPT-4o) and improved inference efficiency, gross margin had improved to approximately 35%. However, this remains far below the 70-80% gross margins typical of SaaS companies.

3.4 Risk Factors

OpenAI's S-1 filing discloses a unique set of risk factors:

Governance Risk: OpenAI's non-profit parent (OpenAI Nonprofit) retains governance control over the for-profit entity. This structure — a non-profit board controlling a publicly traded company valued at $852 billion — is unprecedented in public markets and may trigger investor concerns about corporate governance.

Technology Competition Risk: The rise of open-source models is eroding OpenAI's pricing power. DeepSeek V4-Flash, available for free under the MIT license, surpasses GPT-4o on multiple benchmarks. If open-source models continue to keep pace, OpenAI's pricing premium will be difficult to maintain.

Legal Litigation Risk: OpenAI faces multiple copyright infringement lawsuits — including from the New York Times, multiple authors, and class actions over code repositories. While the company asserts a "fair use" defence, the uncertainty of legal outcomes constitutes a potentially material liability.

→ Return to TOC | → Next: Titans Compared

Chapter 4: Titans Compared — Business Models, Risks, and Valuation Logic

4.1 Business Model Differences

While Anthropic and OpenAI compete in the large language model market, their business models differ fundamentally:

| Dimension | Anthropic | OpenAI |

|---|---|---|

| Core Positioning | Safety-first enterprise AI | General AI platform |

| Target Customers | Large enterprises, government, financial institutions | Consumers, developers, enterprises |

| Pricing Strategy | Premium (Fable 5 at $15/M tokens) | Tiered (free to $200/month) |

| Ecosystem Strategy | Closed API, curated partners | Open API + ChatGPT consumer brand |

| AI Safety Philosophy | Constitutional AI (rule-driven alignment) | RLHF + safety training at scale |

| Open Source Stance | Does not open-source core models | Does not open-source (but early GPT-2 was open-sourced) |

4.2 Valuation Multiple Comparison

Based on 2025 financial data:

Anthropic: $965B valuation ÷ $10B ARR (end of 2025) = 96.5x ARR OpenAI: $852B ÷ $24B ARR (estimated end of 2025) = 35.5x ARR

The valuation multiple gap is enormous. Anthropic's higher multiple reflects the market's premium for its growth rate (ARR growing from $10B to $47B in six months) and differentiated positioning. OpenAI's lower multiple reflects the market's discount for governance risk, competitive pressure, and legal exposure.

However, in absolute terms, Anthropic ($965B) has surpassed OpenAI ($852B) — unimaginable just one year ago. In early 2025, OpenAI's valuation (~$300B) was roughly 5x Anthropic's (~$60B). The reversal reflects how quickly the market is reassessing the AI competitive landscape.

4.3 Worst-Case Scenario Analysis

For each company's most significant risk, we conducted scenario analysis:

Anthropic's Worst Case: A major safety incident involving Claude 4/Fable 5 (e.g., jailbreak leading to sensitive information leakage), triggering regulatory penalties and enterprise customer churn. In this scenario, Anthropic's revenue could decline 40-60%, with valuation potentially falling to $200-300 billion — consistent with its current 10x ARR multiple.

OpenAI's Worst Case: Adverse copyright ruling, with courts finding that AI training on copyrighted material does not constitute fair use. This could require OpenAI to pay tens of billions in damages and restrict the training data scope for future models. Combined with open-source model competitive pressure, valuation could fall to $150-250 billion.

4.4 Merger Possibility

Market speculation occasionally surfaces about a potential Anthropic-OpenAI merger. While this is extremely unlikely in the near term (the two companies have fundamentally different cultures and missions), the financial logic is compelling: a combined entity would have the largest model portfolio, the broadest customer base, and the strongest negotiating leverage. However, antitrust regulators would almost certainly block such a merger — the combined market share of the two AI leaders would trigger global regulatory scrutiny.

→ Return to TOC | → Next: SpaceX

Chapter 5: SpaceX — The $1.77 Trillion Elephant in the Room

While this report focuses on the AI IPO wave, it cannot ignore SpaceX — not only is it the largest IPO of 2026 (at a $1.77 trillion valuation), but it also forms deep capital market interactions with the AI IPOs.

5.1 Three-Track Listing

SpaceX's IPO differs from Anthropic's and OpenAI's in its "three-track" strategy:

Institutional Allocation: The majority of shares are allocated to institutional investors, including existing shareholders such as Fidelity, Valor Equity Partners, and Founders Fund.

Retail Channel: SpaceX broke new ground by announcing it would make shares available to retail investors through five brokerage platforms: Charles Schwab, Fidelity, Robinhood, SoFi, and E-Trade by Morgan Stanley. This is extremely rare for large tech IPOs — the typical institutional/retail allocation ratio is 95:5, while SpaceX's retail allocation is expected to reach 10-15%. This strategy both rewards SpaceX's massive fan base and establishes a broader shareholder base in the public market.

Employee Shares: SpaceX employees (including production line workers) will receive special share allocation plans. Given SpaceX's valuation, this could create thousands of new millionaires.

5.2 SpaceX and AI IPO Capital Competition

SpaceX, Anthropic, and OpenAI will collectively absorb over $300 billion from public markets in the second half of 2026 (based on estimated dilution ratios from IPO share issuance). This affects global capital markets in several ways:

Capital Absorption Effect: The $300 billion capital demand is equivalent to approximately 60% of the entire US IPO market in 2025. This means other companies planning to go public in the second half of 2026 will face significantly greater difficulty in raising capital.

Valuation Benchmark Effect: These three companies will establish public market valuation benchmarks for their respective sectors (AI and space). These benchmarks will influence financing pricing across the entire industry — for better or worse.

Investor Attention Dilution: Even the most dedicated technology investors will struggle to deeply analyse three completely different (yet equally complex) companies simultaneously. This could lead to insufficient analysis depth, increasing the risk of mispricing.

→ Return to TOC | → Next: Capital Rotation Effects

Chapter 6: Capital Rotation Effects — Impact on FAANG and Tech Markets

Figure 3: Structural capital migration from FAANG to AI-native companies.

6.1 Capital Migration from FAANG to AI-Native Companies

The Nasdaq's 4% decline on June 5, 2026 is not an isolated event — it reflects a structural migration of capital from existing tech giants to AI-native companies.

When Anthropic and OpenAI go public at 30-100x ARR multiples, they will face direct valuation comparisons with FAANG. Microsoft (30x P/E, approximately 12x ARR multiple), Google (22x P/E, approximately 6x ARR multiple), and Amazon (40x P/E, approximately 3x ARR multiple) will appear cheap by comparison. If AI-native companies can sustain higher growth premiums in public markets, fund managers will be forced to rebalance their technology portfolios — reducing FAANG positions and increasing allocations to AI-native companies.

6.2 NVIDIA's Unique Position

NVIDIA is simultaneously the greatest beneficiary and potential victim of this AI IPO wave. On one hand, Anthropic's and OpenAI's GPU demand forms the backbone of NVIDIA's revenue — the two companies collectively operate over 1.5 million GPUs. On the other hand, if AI IPO proceeds are partially allocated to custom chip development (Anthropic is already working with Broadcom on ASICs, OpenAI is collaborating with Microsoft on AI chip design), NVIDIA will face long-term competition from its largest customers.

NVIDIA's early June announcement of a Physical AI partnership with Unitree — integrating the Omniverse platform into Unitree's humanoid robots — can be interpreted as NVIDIA's diversification strategy in response to the AI IPO wave: reducing dependence on the LLM/cloud AI market and expanding into robotics and edge AI.

6.3 Deeper Impact of the Crowding-Out Effect

The capital absorption effect of AI IPOs extends beyond technology stocks into the venture capital market. In 2025, global venture capital totalled approximately $350 billion, with roughly 40% ($140 billion) flowing into the AI sector. IPOs of Anthropic and OpenAI will return tens of billions to their venture investors (including Sequoia, Andreessen Horowitz, Khosla Ventures, and others). These returns will be reinvested into the venture ecosystem — but not evenly distributed. Funds that benefited from AI IPO returns will have more capital to invest in the next wave of AI startups, while funds that missed these returns will face a much more difficult fundraising environment.

This means capital concentration in AI will further increase — top-tier AI startups (such as xAI, Mistral, Cohere) will receive more funding, while other sectors (biotech, climate tech, hardware) will face greater financing difficulties.

→ Return to TOC | → Next: AI IPO as Industry Signal

Chapter 7: AI IPO as Industry Signal — How Public Markets Price AI Maturity

7.1 The Transition from "Technology" to "Infrastructure"

The IPOs of Anthropic and OpenAI are not just financing events — they are signals of industry maturity. When a company can raise capital from public markets rather than venture capital, it means its business model has passed the most rigorous due diligence — public market audit, disclosure, and regulatory requirements far exceed those of private markets.

The AI industry is undergoing a three-stage maturity transition:

Stage 1: Technology Development (2015-2023) — Exponential improvement in model capability, but unclear business models. OpenAI's revenue in 2023 was only $1.6 billion against operating costs exceeding $5 billion. Funding at this stage relied entirely on venture capital and strategic investors.

Stage 2: Commercial Validation (2024-2025) — GPT-4 and Claude 3 demonstrated AI's commercial value, accelerating enterprise adoption. OpenAI's ARR grew from $1.6 billion in 2023 to $24 billion in 2025; Anthropic grew from near zero to $10 billion. Companies began generating meaningful revenue but remained unprofitable.

Stage 3: Scaled Public Listing (2026-) — IPOs provide long-term capital and acquisition currency. Public market price discovery will establish market-based pricing benchmarks for AI models, computing power, and talent.

7.2 How Public Markets Price AI Companies

Traditional valuation frameworks (DCF, P/E, EV/EBITDA) face fundamental challenges in assessing AI companies. AI companies have unique characteristics:

Extreme Capital Intensity: Anthropic and OpenAI's capital expenditure (primarily GPUs and data centres) exceeds 50% of revenue, far above the 10-20% typical of SaaS companies. This means even as gross margins improve, free cash flow generation will take longer.

Uncertain Network Effects: Whether AI models exhibit network effects (more users generating more data, which improves the model) remains debatable. If the data flywheel exists, first-mover advantages self-reinforce and the market tends toward monopoly. If the data flywheel does not exist (because synthetic data and reinforcement learning can substitute for real user data), the market will sustain multiple competitors.

Technology Substitution Risk: Technology iteration in AI is extremely rapid. What was considered the most advanced model 18 months ago (GPT-4) has now been surpassed by open-source models. In this environment, investors cannot assume current technological advantages will persist.

Therefore, market pricing of AI IPOs may follow an "option pricing" logic — investors are not buying current cash flows but call options on future AI market dominance. This explains why AI companies can go public at 30-100x ARR multiples, while typical SaaS companies trade at 5-10x ARR.

→ Return to TOC | → Next: Regulation and Antitrust

Chapter 8: Regulation and Antitrust — SEC, EU AI Act, and AI Governance

8.1 SEC AI Disclosure Requirements

Anthropic's and OpenAI's S-1 filings provide the SEC an opportunity to establish disclosure standards for AI companies. The SEC has expressed concern about the following areas:

Quantitative Model Risk Disclosure: The SEC requires disclosure of AI model error rates, bias test results, and safety incident records. This is a novel compliance requirement for Anthropic and OpenAI — traditional software companies are not required to disclose product "error rates" or "bias test results."

Computing Resource Dependence: The SEC requires disclosure of dependence on specific hardware vendors (NVIDIA) and the risk of supply chain disruption. Given US export controls on AI chips to China, this disclosure is critical for assessing geopolitical risk.

Intellectual Property Risk: The SEC requires disclosure of the potential impact of copyright litigation, including the sources and usage rights of training data. This may include quantifying how much copyrighted material was used in model training.

8.2 EU AI Act Global Impact

The EU AI Act began enforcement of compliance requirements for high-risk AI systems on June 2, 2026. For general-purpose AI model providers like Anthropic and OpenAI, the Act requires:

Transparency Reporting: Disclosure of training data, computing resources, and performance evaluations. This partially overlaps with SEC disclosure requirements, but EU requirements are more detailed, including energy consumption and carbon emissions data.

Risk Management Systems: Establishment of systematic risk identification, assessment, and mitigation processes. For general-purpose AI models, this includes model misuse risks (such as generating disinformation or cyber attack tools) and systemic risks (such as impact on entire industries).

Copyright Compliance: The EU AI Act requires AI companies to demonstrate copyright compliance of their training data. This creates transatlantic regulatory coordination with OpenAI's ongoing US copyright litigation — if a US court finds OpenAI infringing copyright, EU regulators could act on the same facts.

Both Anthropic and OpenAI have registered under the EU AI Act. For both companies, compliance with the EU market (representing approximately 20-25% of global AI spending) is a prerequisite for going public, not an option.

8.3 Antitrust Scrutiny

The IPOs of Anthropic and OpenAI will trigger antitrust regulator concern about AI market concentration.

The US Federal Trade Commission (FTC) has already begun investigating competition in the AI market, focusing on: whether strategic investments by the three major cloud providers (AWS, Azure, GCP) in AI startups create market foreclosure; whether NVIDIA's dominant position in the AI chip market (~80% market share) constitutes a monopoly; and whether Microsoft's investment in OpenAI and Google's investment in Anthropic reduce competition.

The European Commission is conducting similar investigations. The EU's position is tougher — it has already requested detailed information from Microsoft and Google about their AI investments and has hinted at designating large language models as "core platform services" under the Digital Markets Act (DMA).

→ Return to TOC | → Next: Post-IPO Landscape

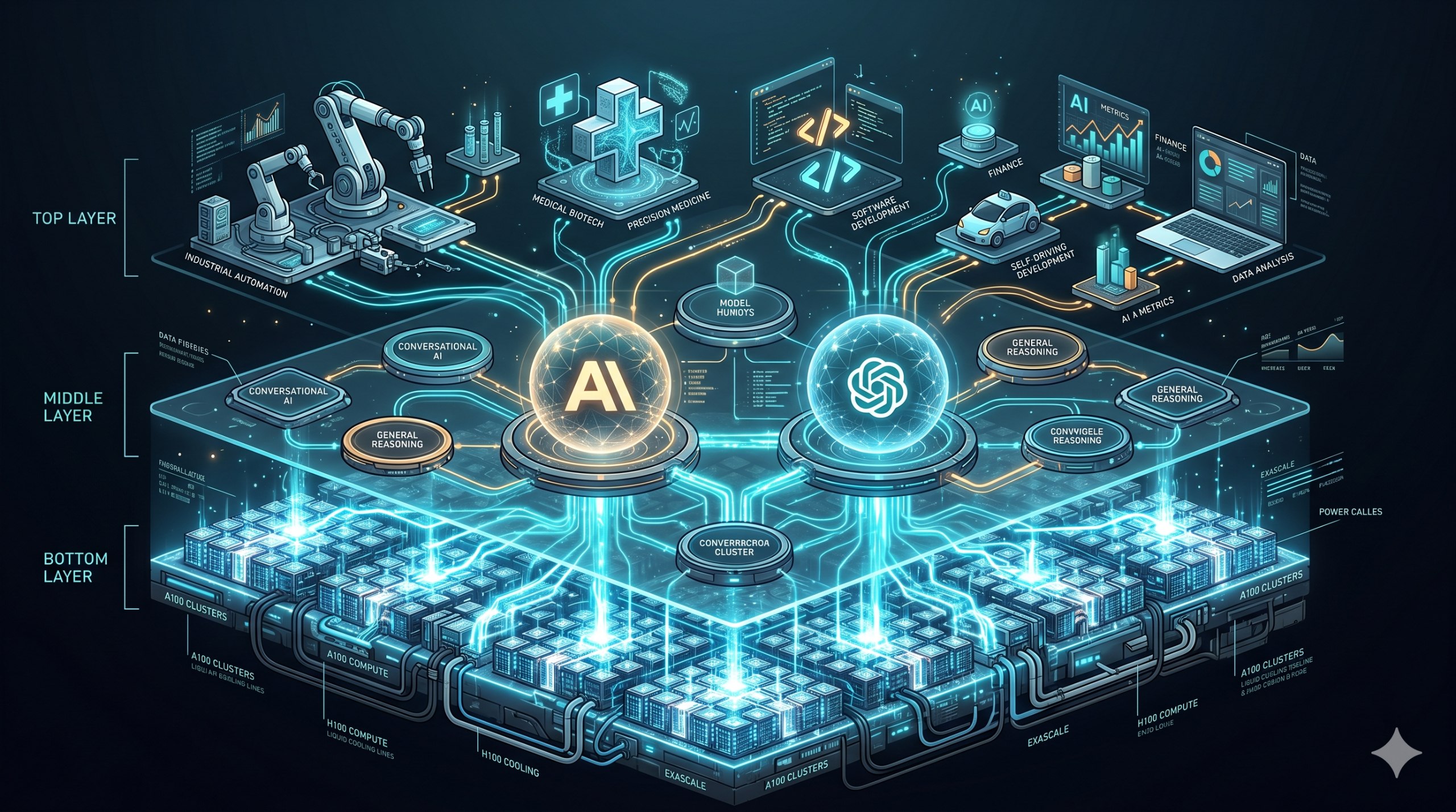

Chapter 9: The Post-IPO AI Landscape — Winners, Losers, and a New Ecosystem

Figure 4: The three-layer AI ecosystem architecture in the post-IPO era.

9.1 Short-Term Winners

Existing Shareholders and Employees: IPOs of Anthropic and OpenAI will create thousands of millionaires and dozens of billionaires. Anthropic's Dario and Daniela Amodei and OpenAI's Sam Altman will become among the wealthiest people on earth.

Venture Capital Funds: Sequoia, Andreessen Horowitz, Khosla Ventures, and other funds will achieve hundreds of times return on their investments from both companies' IPOs. These returns will provide strong fundraising momentum for their next funds.

NVIDIA: Most capital raised from AI IPOs will be deployed into computing infrastructure expansion, meaning more GPU orders. Even if customers begin developing custom chips, NVIDIA will remain the absolute dominant force in AI computing for the next 3-5 years.

9.2 Medium-Term Losers

Second-Tier AI Startups: Once Anthropic and OpenAI have access to tens of billions of dollars in public market capital, they can further strengthen their competitive advantages through acquisitions and hiring. This places unlisted AI startups (including xAI, Mistral, Cohere, and Adept) under greater funding and talent competition pressure.

Open-Source AI Ecosystem: While open-source model performance is improving rapidly (DeepSeek V4-Flash already surpasses GPT-4o on multiple benchmarks), the open-source community lacks the scaled capital investment of Anthropic and OpenAI. Over the next 2-3 years, open-source models may fall behind well-capitalised closed models at the frontier of performance.

Traditional SaaS Companies: AI-native IPOs will redefine valuation standards across the software industry. Traditional SaaS companies like Salesforce, Workday, and ServiceNow face commoditisation pressure from AI capabilities — when AI assistants can automatically handle CRM data entry or HR screening, these companies' high-margin business models will face erosion.

9.3 Structural Changes in the AI Ecosystem

The post-IPO AI ecosystem may take the following shape:

"Three-Layer" Architecture: The bottom layer is cloud infrastructure (AWS, Azure, GCP, and NVIDIA), the middle layer is AI model platforms (Anthropic, OpenAI, Google DeepMind), and the top layer is AI applications (Microsoft Copilot, Salesforce Einstein, custom applications). Profit distribution among these three layers will be the most important business dynamic of the next decade.

Platform Competition: Anthropic and OpenAI will expand from model providers to platform companies. Anthropic is already developing Claude's application platform — allowing third-party developers to build applications on Claude, similar to OpenAI's GPT Store. Platform economics differ from model economics: platforms have near-zero marginal costs, while models have computing costs proportional to usage.

Geopolitical Dimension: The post-IPO AI landscape will be deeply influenced by geopolitics. US AI chip export controls are driving China to build an independent AI ecosystem — the formation of the DeepSeek Alliance exemplifies this trend. Over the long term, the global AI market may split into a "US ecosystem" (Anthropic, OpenAI, Google) and a "China ecosystem" (DeepSeek, Baidu, Alibaba, Tencent), with the two ecosystems diverging increasingly in technology stack, regulatory framework, and business model.

→ Return to TOC | → Next: Conclusion

Chapter 10: Conclusion — Investing in the AI Infrastructure Transition

The simultaneous IPOs of Anthropic, OpenAI, and SpaceX are not just a 2026 capital markets event — they represent a historic transition of the technology industry from "venture-capital-driven innovation" to "public-market-driven infrastructure construction."

For Anthropic and OpenAI, the IPO is not an endpoint but a beginning. Public markets will provide them with the capital they need — not for laboratory technology research, but for scaled infrastructure construction. Hundreds of billions of dollars will be converted into more GPUs, larger data centres, and broader global operations networks. AI will transform from a "what can it do" technology question to a "how to scale it" engineering question.

For investors, the AI IPO wave poses a fundamental question: how do you price an industry that is still evolving rapidly technologically, not yet profitable commercially, but already strategically indispensable? Traditional valuation frameworks cannot provide satisfactory answers — just as with internet companies in the late 1990s, AI company valuations are based more on bets on future dominance than on discounted present cash flows.

Our long-term view on the AI IPO wave is cautiously optimistic. The reason for optimism: AI is not hyping a non-existent market — it has already generated measurable productivity improvements in code generation, customer service, drug discovery, and scientific research. The reason for caution: when an industry's total investment ($180 billion for OpenAI + approximately $100 billion for Anthropic) far exceeds its current revenue (approximately $70 billion combined ARR), the timeline for capital returns will be longer than the most optimistic forecasts.

But one thing is certain: AI infrastructure construction is proceeding at "space programme scale," and public markets — not governments or venture capital — will provide the primary funding for this construction. This has never happened before in technology history, and it is the deepest meaning of the 2026 AI IPO wave.

References

- Anthropic. "Anthropic raises $65B in Series H funding at $965B post-money valuation." May 28, 2026.

- OpenAI. "OpenAI raises $122 billion to accelerate the next phase of AI." March 31, 2026.

- Fortune. "Anthropic confidentially files for IPO after a $965 billion valuation." June 1, 2026.

- CNBC. "OpenAI IPO: Confidential S-1 filed, September target." June 8, 2026.

- CNBC. "SpaceX IPO explained: The price is set, but retail allocation still up in the air." June 9, 2026.

- Forbes. "Here's How To Invest In SpaceX, OpenAI and Anthropic IPOs—And The Big Risks." June 4, 2026.

- TechCrunch. "Anthropic raises $65 billion, nears $1T valuation ahead of IPO." May 28, 2026.

- EU AI Act Official Journal. "Regulation (EU) 2024/1689."

- Financial Express. "AI weekly roundup." June 7, 2026.

- CNBC. "Anthropic tops OpenAI as most valuable AI startup." May 28, 2026.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Data and timestamps are accurate as of the publication date and may change with subsequent developments. Neither the author nor POC.HK assumes any liability for losses arising from the use of this information.